You make $50,000 a year. You’re tired of renting. And somewhere in the back of your head, you’ve started doing the math – can I actually pull this off?

Here’s the truth: yes, you probably can. But the number most people land on is wrong – because they only calculate the mortgage and ignore everything else. By the end of this, you’ll know exactly what you can afford, what the bank will approve you for (different things, by the way), and what costs will quietly wreck your budget if you’re not looking for them.

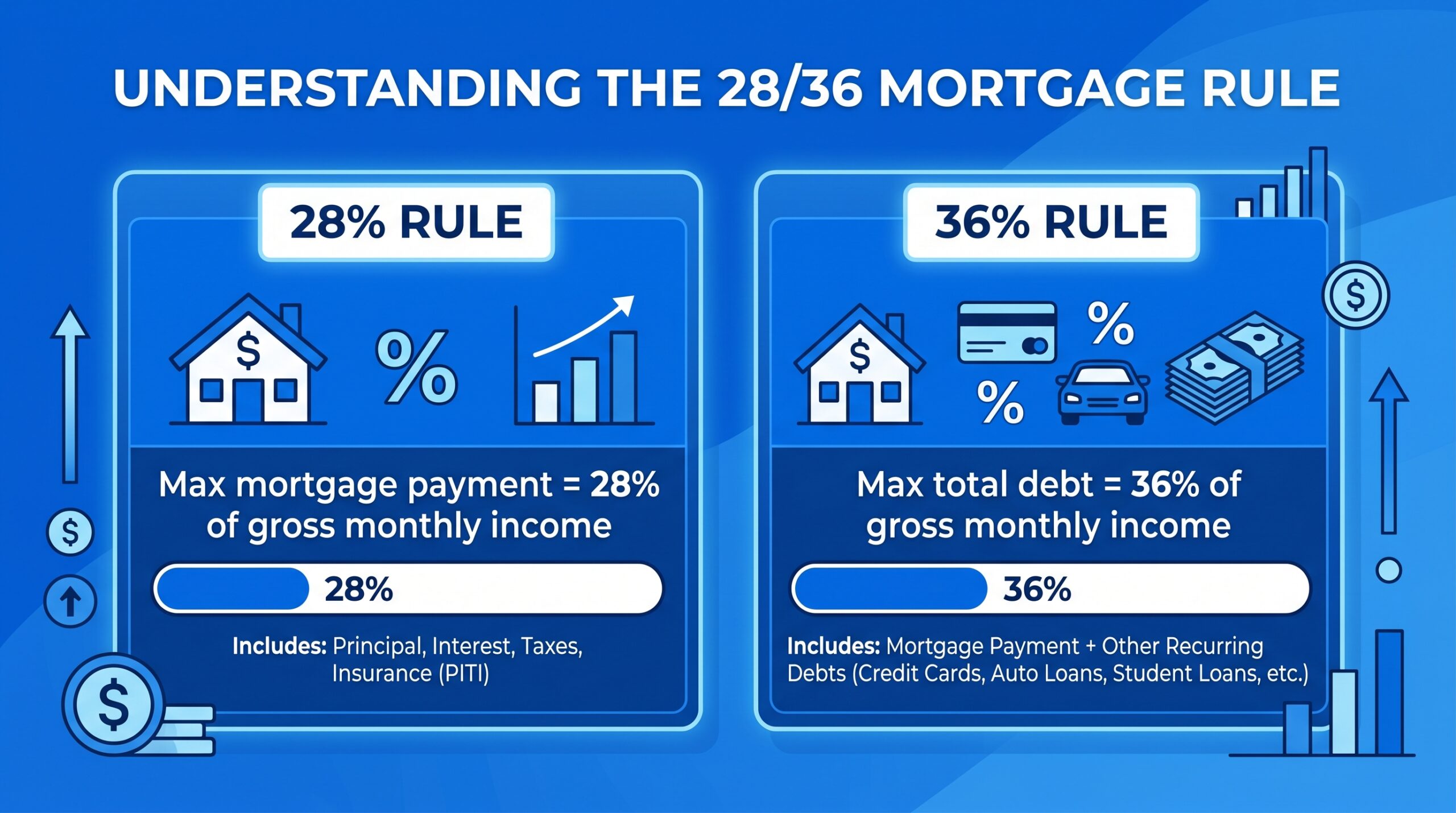

The Rule Lenders Use – And It’s Not What You Think

Banks don’t just look at your salary and say yes or no. They run two filters. Both of them. This standard, known as the 28/36 rule, is used by virtually every mortgage lender in the US.

The 28% Rule

Your monthly mortgage payment – principal + interest – shouldn’t exceed 28% of your gross monthly income. Not take-home. Gross. Before taxes.

On $50,000/year, your gross monthly income is $4,167.

28% of that = $1,167/month. That’s your ceiling.

The 28/36 Rule – This Is the One That Bites People

Here’s where it gets real. Lenders look at your total monthly debt – car loans, student loans, credit cards, everything – and say it can’t exceed 36% of your gross monthly income.

36% of $4,167 = $1,500/month for ALL debt combined.

So if you’re paying $400/month on a car loan? Your mortgage budget just dropped to $1,100/month. You didn’t change your salary. You didn’t change the house. Just that one number quietly shrunk what you can borrow.

Most first-time buyers never see this coming.

Okay, So What Home Price Does $1,167/Month Actually Buy?

Let’s use real 2025 numbers. Mortgage rates right now are hovering around 6.7% on a 30-year fixed loan. Here’s what different down payments get you at that rate:

| Down Payment | Home Price You Can Afford |

|---|---|

| 3% (FHA minimum) | ~$152,000 |

| 10% | ~$168,000 |

| 20% (no PMI) | ~$185,000 |

That jump from 10% to 20% isn’t just about a higher home price. It eliminates Private Mortgage Insurance or PMI — a monthly fee lenders charge when your down payment is under 20%.. PMI typically adds $80-$160/month on a loan this size. Get rid of it and suddenly your same $1,167 budget stretches further.

You can also use the simple 2.5x rule as a quick gut-check: multiply your salary by 2.5.

$50,000 × 2.5 = $125,000

Conservative, but safe. Most buyers on a $50k salary realistically land somewhere between $130,000 and $190,000 depending on their debt and down payment situation.

Meet Jake – This Is What It Actually Looks Like

Jake is 29. He works in logistics in Columbus, Ohio and earns $50,000/year. He has one car loan at $320/month and no student debt. He’s been saving for two years and has $14,000 set aside for a down payment.

Here’s how his numbers play out:

- Gross monthly income: $4,167

- Max total debt allowed (36%): $1,500

- Minus car payment: −$320

- Mortgage budget: $1,180/month

With $14,000 down (roughly 9% on a $155,000 home) at 6.7% over 30 years, Jake’s looking at a monthly payment of about $1,140 – just inside his budget.

He’s not buying in San Francisco. But Columbus? He’s got solid options in good neighborhoods.

The Costs Nobody Warns You About

Here’s the part that surprises almost everyone.

The mortgage payment is just one line item. Your actual monthly housing cost includes:

- Property taxes – usually 1-2% of home value per year. On a $160,000 home, that’s $130-$270/month added to your costs.

- Homeowner’s insurance – typically $800-$1,500/year, or $65-$125/month.

- PMI – if your down payment is under 20%, add roughly 0.5-1% of the loan annually.

- HOA fees – not always, but condos and planned communities can charge $100-$400/month.

- Maintenance – this one people always skip. Financial advisors recommend setting aside 1% of your home’s value each year for repairs. On a $160,000 home, that’s $1,600/year – or $133/month you should be mentally budgeting.

Add all of that up and a “$1,167 mortgage payment” can easily become $1,600-$1,800 in total monthly housing costs.

Does that change your plan? It should. Not to scare you – just to make sure you’re buying with eyes open.

What’s YOUR Number? Find Out in 30 Seconds

Jake’s situation is one version. Yours is different. Different debt, different down payment, different location with different property taxes.

That’s exactly why a mortgage calculator exists – to stop guessing and start knowing.

👉 Calculate Your Mortgage on NumiCalc – Free, Instant, No Signup

Plug in your home price, down payment, interest rate, and loan term. You’ll see your exact monthly payment broken down – principal, interest, and total cost over the life of the loan.

Takes 30 seconds. Could save you from a 30-year mistake.

4 Ways to Afford More Without Earning More

Salary is fixed. But your buying power isn’t.

Kill existing debt first. Paying off a $300/month car loan before house hunting adds that $300 straight back into your mortgage budget. That can mean $30,000-$40,000 more in home price.

Build your credit score. A score above 740 gets you the best rates. The difference between a 680 and a 750 credit score can be 0.5-0.75% on your interest rate – which sounds small but adds up to $15,000-$25,000 over 30 years.

Consider FHA loans. Government-backed mortgages that allow down payments as low as 3.5%, more flexible on credit requirements. Built for people in exactly your situation.

Buy in a lower property-tax state. The same $160,000 home costs you $200/month more in property taxes in New Jersey versus Alabama. Location is a financial decision, not just a lifestyle one.

The Bottom Line

On $50,000/year with average debt, you’re realistically looking at homes in the $130,000-$185,000 range. The exact number depends on what you owe, what you’ve saved, and where you want to live.

The bank might approve you for more. Don’t let that fool you – approved doesn’t mean comfortable.

Know your real number. Then go find the house.

👉 Run Your Numbers on NumiCalc’s Free Mortgage Calculator

This article is for informational purposes only and does not constitute financial or mortgage advice. For guidance specific to your situation, consult a licensed mortgage professional.